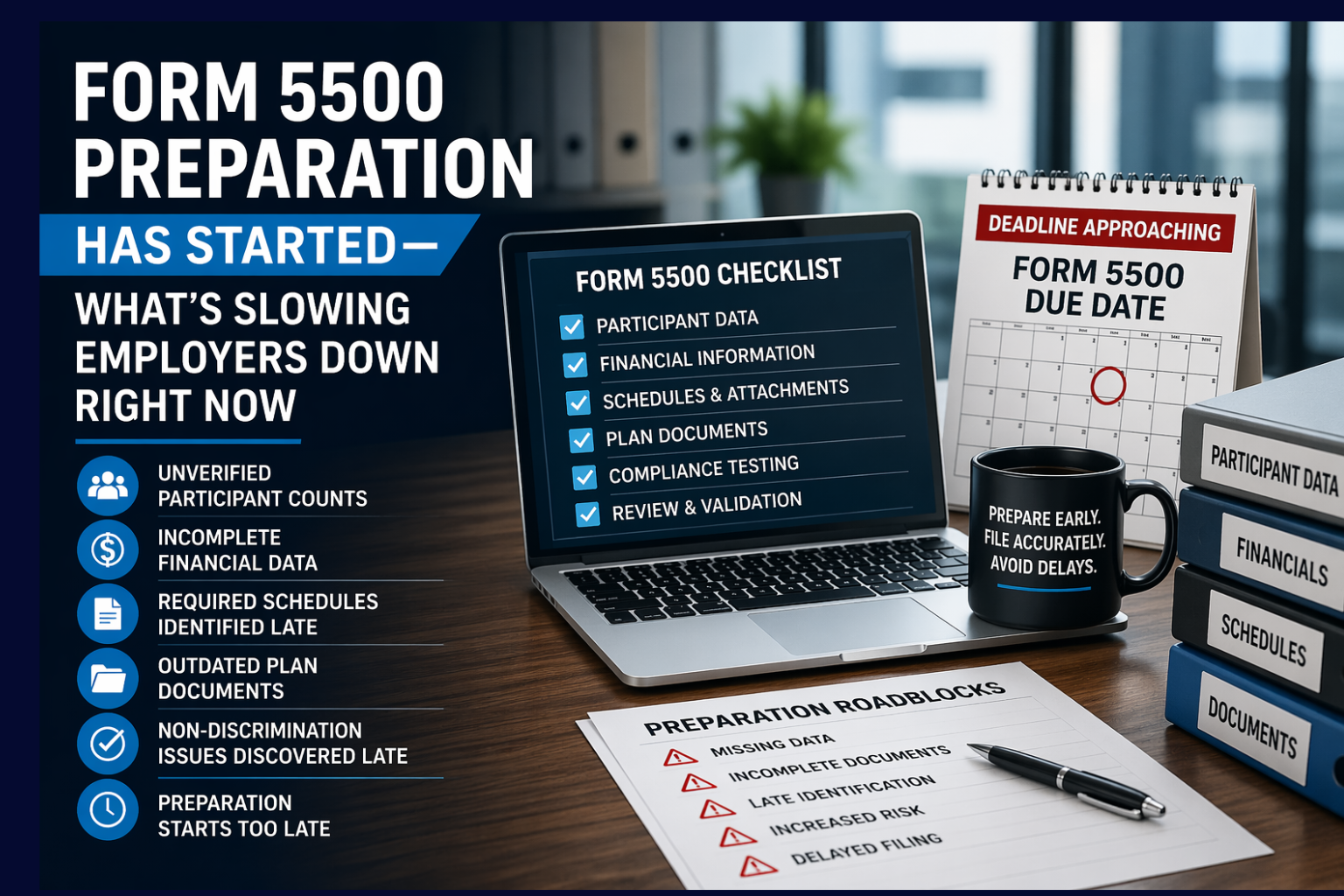

Why Form 5500 Filing Slows Down Once Preparation Begins

Preparation Exposes Filing Gaps Form 5500 preparation exposes filing gaps quickly. Missing records, incomplete data, and outdated documentation interrupt preparation as soon as review begins. Most filing slowdowns already existed before preparation started.Preparation does not create filing problems. [...]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}